Accounting For No Par Value Shares

No Par Stock Journal Entry In Accounting Double Entry Bookkeeping

Accounting For Common Stock Issuances No Par Value Youtube

No Par Value Stock Explanation Journal Entries And Example

Par Value And No Par Value Stock Youtube

Common Stock Issued With Par Value Vs No Par Value Accounting

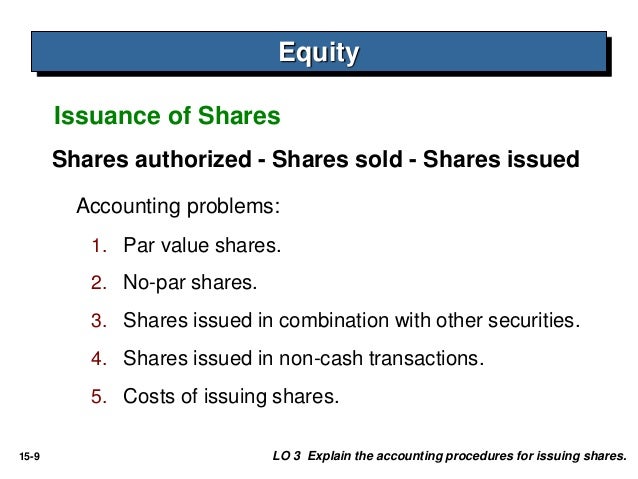

7 Accounting For Equity

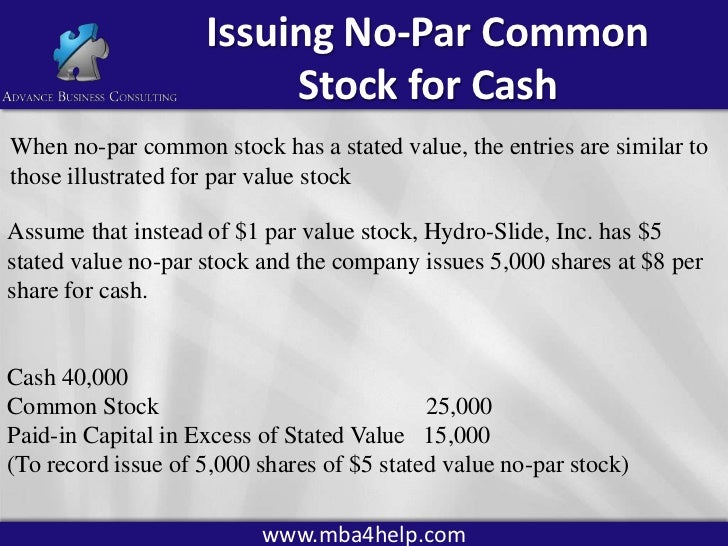

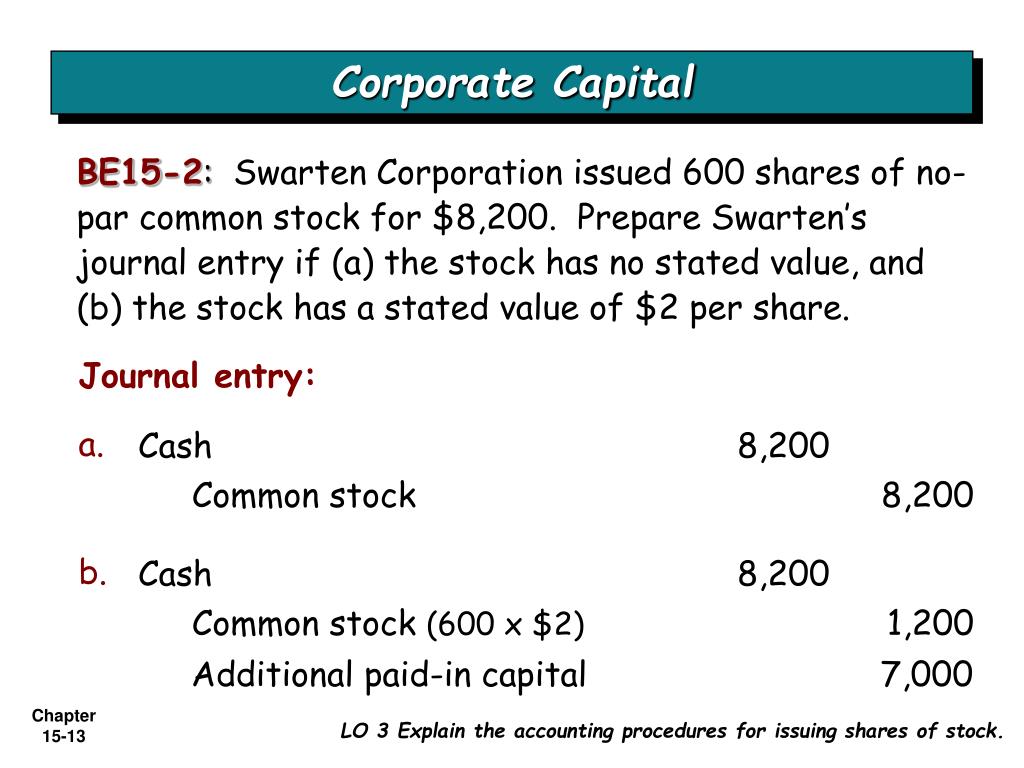

No par value stock is shares that have been issued without a par value listed on the face of the stock certificate historically par value used to be the price at which a company initially sold its shares.

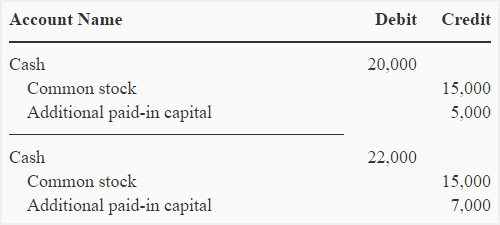

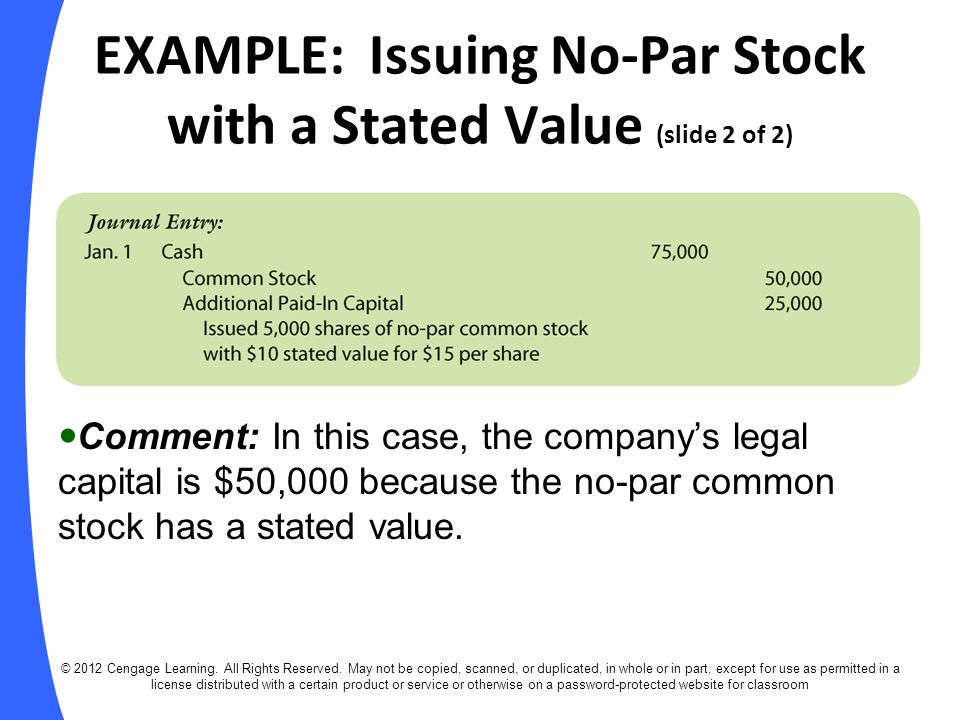

Accounting for no par value shares. Par value of shares also known as the stated value per share is the minimal shares value as decided by the company which is issuing such shares to the public and the companies then will not sell such type of shares to the public below the decided value. No par stock is stock issued without a par value. Journal entry for issuing no par value stock. No par value stock sometimes called no par stock is a class of stock that was never assigned a par value or stated value.

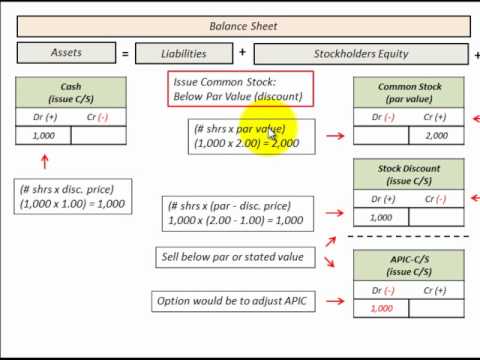

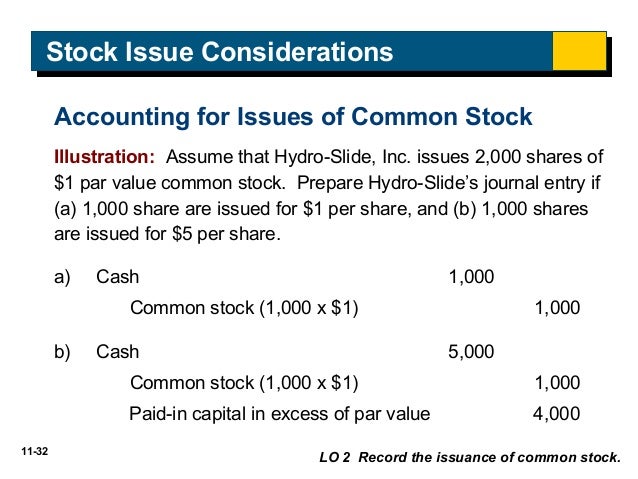

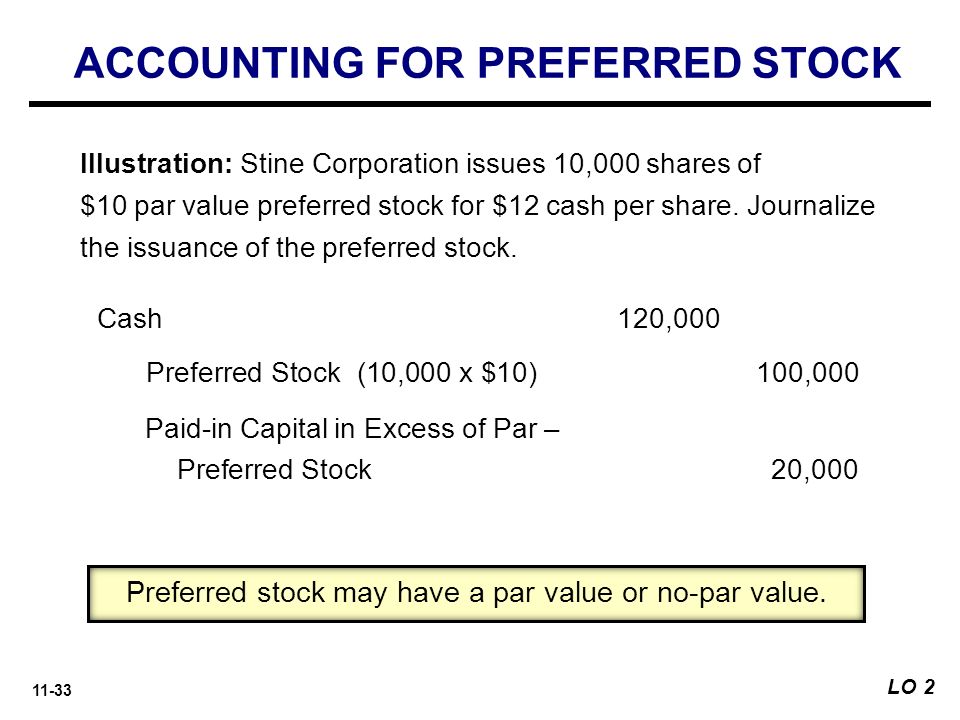

From an accounting standpoint the par value of an issued share of common stock must be recorded in an account separate from the amount received over and above the amount of par value. In other words it is the share nominal amount 1 0 1 or 0 001 mentioned on the stock certificate at the time. Learn shares issued at premium here. Par value for stock.

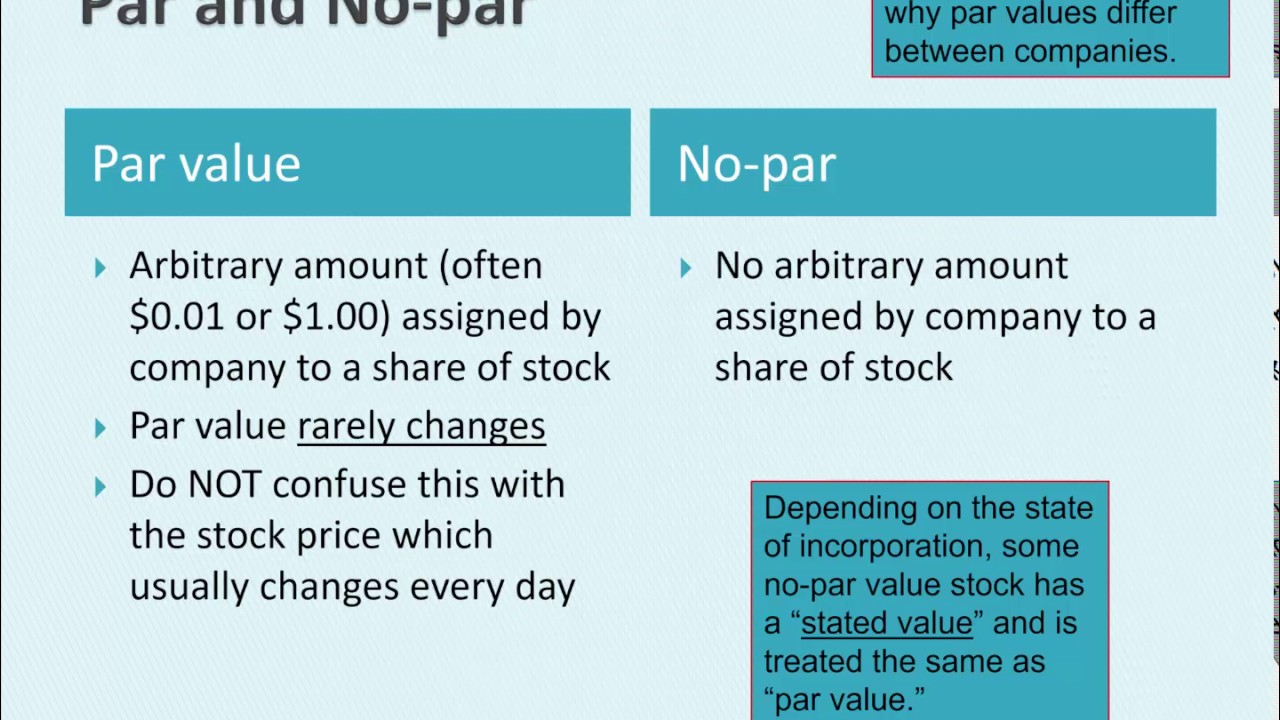

The intent behind the par value concept was that prospective investors could be assured that an issuing company would not issue shares at a price below the par value. What is par value of share. No par value stock prices are determined by the amount that investors are willing to pay for the stocks on the open. Par value is the stock price stated in a corporation s charter.

The shares will be at par is when the shares are sold at their nominal value. Although prohibited in many countries the issuance of no par value stock is allowed in some states of usa. No par value stock as the name implies is a type of stock that does not have a par value attached to each of its share unlike par value stock no par value stock certificate does not have a per share value printed on it. In the past companies issued shares with significant par values such as 10 00 per share leading to confusion between this arbitrarily assigned amount and the actual market value of the shares with which it has no link.

For example if a corporation issues 100 new shares of its common stock for a total of 2 000 and the. Normally when a business is incorporated the corporate charter assigns a par value or base value for every share that will be issued. However par value is now usually set at a minimal amount such as 0 01 per share since some state laws still require that a company cannot. A par value is a nominal or face value given to a share in the stock of a company authorized by its charter.

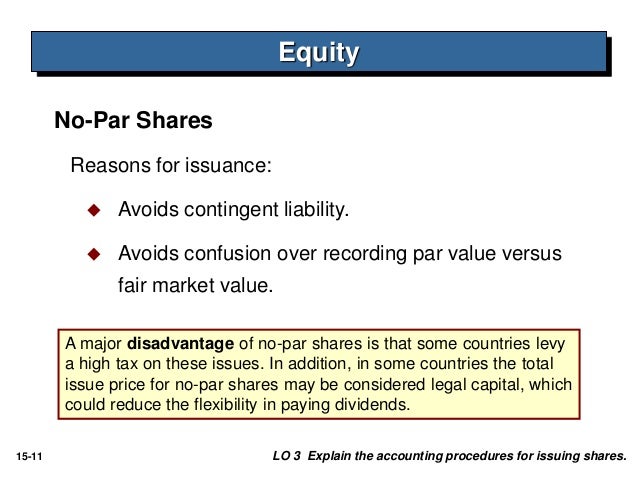

So the par value on common stock is a legal consideration. A no par value stock is issued without the specification of a par value indicated in the company s articles of incorporation or on the stock certificate itself. Shares sold at a premium cost more than their nominal value and the amount in excess of the face value is the premium.

Ppt C H A P T E R 15 Powerpoint Presentation Free Download Id

Nobles Fin5 Ppt 13

Chapter 11 Stockholders Equity Ppt Download

Par Value And No Par Value Stock Youtube

12 1 Capital Stock Transactions

Par No Par Stock Youtube

Share Capital

7 Accounting For Equity

Acc102 Chap11 Publisher Power Point

Share Capital

Chapter 11 Stockholders Equity Ppt Download

Https Mgmt026 Files Wordpress Com 2014 11 Mgmt 026 Chapter 13 Hw Pdf

11 Reporting And Analyzing Stockholders Equity Ppt Download